Central Oregon’s geography and weather patterns create genuine flood risks that many homeowners underestimate. Standard homeowners insurance typically won’t cover flood damage, leaving your property vulnerable without proper protection.

Flood insurance in Central Oregon is essential for anyone in a flood-prone area or simply concerned about water damage. This guide walks you through your options, coverage types, and the straightforward steps to secure the right policy for your home.

What Makes Central Oregon Flood Risk Different

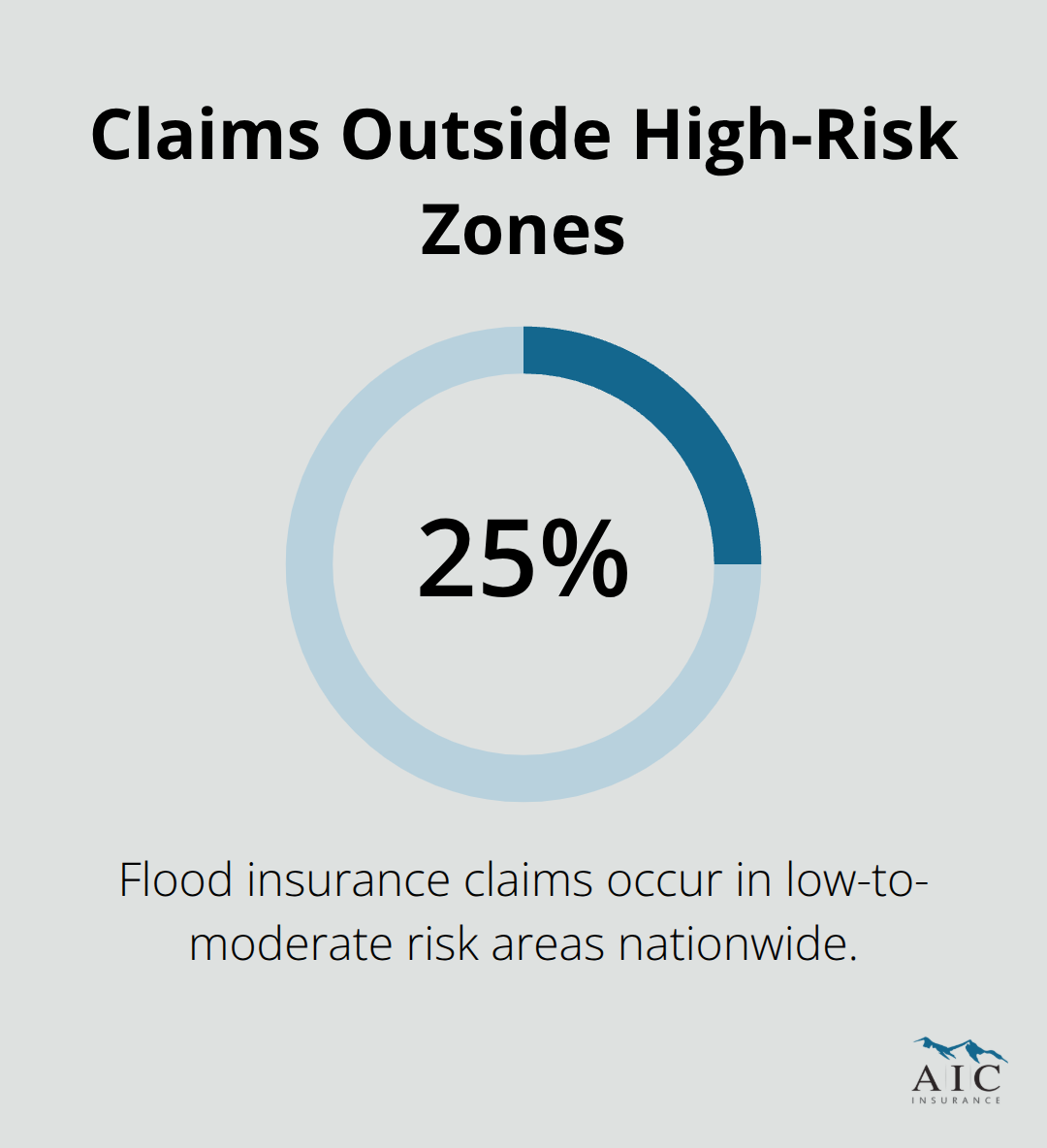

Central Oregon’s flood hazards stem from a specific combination of geography and seasonal weather that differs sharply from other regions. The Deschutes River and its tributaries flood predictably during spring snowmelt and fall-winter precipitation, while rapid development in floodplain areas has intensified runoff and reduced natural water absorption. Flash flooding in canyon areas poses acute risks that standard flood models sometimes underestimate. FEMA’s flood hazard maps identify high-risk zones along these corridors, but the reality extends beyond mapped boundaries-about 25 percent of flood insurance claims nationwide occur in low-to-moderate risk areas, meaning your property faces genuine exposure even if flood zone maps suggest otherwise.

Understanding Your Property’s Actual Flood Risk

Your actual flood risk depends on multiple factors: elevation relative to nearby waterways, soil type, stormwater infrastructure capacity in your neighborhood, and whether your home sits on a slope that channels water downhill during heavy rain. Many Central Oregon homeowners wrongly assume that living outside a designated high-risk flood zone means flood insurance is optional or unnecessary. This misconception costs families thousands in uninsured losses annually. Flood season in Oregon runs from October through March, when precipitation intensifies and snowmelt accelerates, yet most homeowners delay insurance purchases until storms arrive-too late, since standard NFIP policies include a mandatory 30-day waiting period before coverage takes effect.

How Your Property’s Flood Zone Shapes Insurance Requirements

FEMA flood maps categorize properties into zones that determine whether flood insurance is mandatory, recommended, or optional. Properties in high-risk zones (typically labeled A or AE) with federally backed mortgages face mandatory flood insurance requirements, with structural coverage mandated up to $250,000 for single-family residences. Contact your local floodplain administrator to identify your property’s exact zone and understand what that designation means for your coverage obligations. Even if your property sits outside high-risk zones, purchasing flood insurance remains strategically sound-premiums for lower-risk properties are substantially cheaper, and coverage protects against the financial catastrophe of even a single flood event.

Elevation Certificates and Premium Discounts

Your elevation relative to the Base Flood Elevation and your building’s foundation type directly influence both your flood risk and your insurance premium, so obtaining an Elevation Certificate documenting these specifics can unlock discounts and clarify your true exposure. Central Oregon homeowners often underestimate how quickly water accumulates in low-lying yards or basements during heavy precipitation, especially if local drainage systems become overwhelmed. The National Flood Insurance Program offers Increased Cost of Compliance coverage up to $30,000 to help bring damaged buildings into compliance with current floodplain standards after a flood, a critical protection that private policies may not provide equally. Understanding these coverage options and your property’s specific characteristics positions you to make informed decisions about the protection your home actually needs.

Choosing Your Flood Insurance Path

Understanding NFIP Coverage and Your Protection Options

The National Flood Insurance Program dominates Central Oregon’s flood insurance market because it remains the only practical option for most homeowners. NFIP policies cover structural damage to your building and separate contents coverage for personal belongings inside-two distinct protection layers that private insurers rarely match in scope or affordability. Structural coverage protects the foundation, walls, roof, and built-in systems; contents coverage reimburses furniture, electronics, and other possessions. For a single-family residence in a high-risk zone with a federally backed mortgage, you must carry structural coverage equal to your loan amount, capped at $250,000.

Why Standard Homeowners Insurance Falls Short

Standard homeowners insurance explicitly excludes flood damage, no matter how catastrophic the water intrusion. Your homeowners policy covers wind-driven rain through a roof breach but stops the moment water rises from external sources like overflowing rivers, saturated soil, or backed-up storm drains. This gap leaves uninsured homeowners facing six-figure losses that insurance will not touch. The NFIP’s Included Cost of Compliance coverage, part of every policy up to $30,000, handles expenses to bring your rebuilt home into compliance with current floodplain standards-a benefit private policies typically exclude entirely.

How FEMA Calculates Your Premium

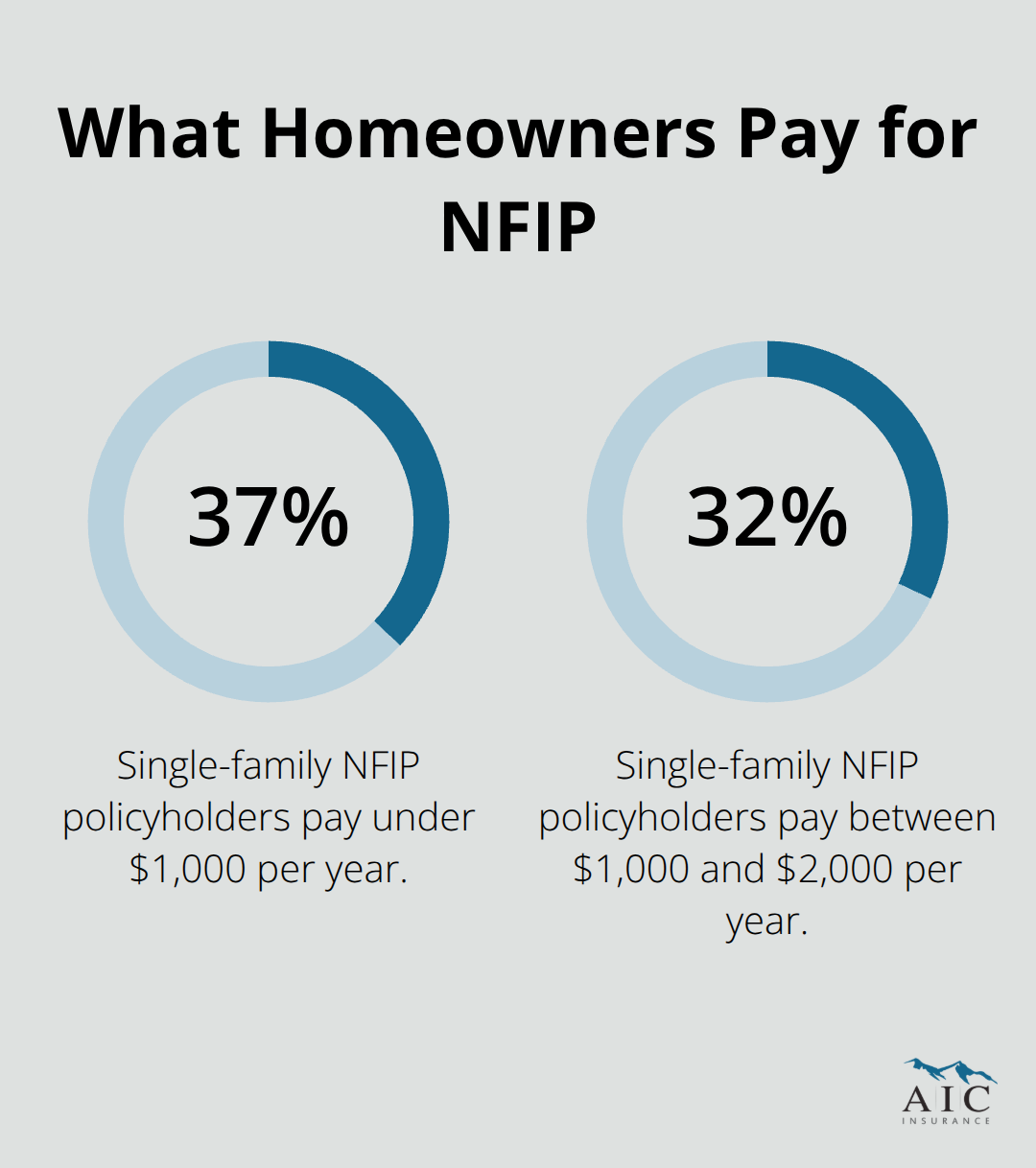

Premium costs reflect your actual risk profile, not just your flood zone designation. FEMA’s Risk Rating 2.0 calculates premiums using property-specific factors: distance from flood sources, elevation relative to base flood levels, foundation type, and first-floor height. Two homes on the same street can pay dramatically different rates based on these variables. About 37 percent of single-family NFIP policyholders nationwide pay under $1,000 annually, while roughly 32 percent pay between $1,000 and $2,000 per year according to FEMA data.

Reducing Your Costs Through Smart Decisions

Central Oregon properties in lower-risk areas often qualify for Preferred Risk Policy rates, substantially cheaper than standard coverage. Annual premium increases are capped at 18 percent as the NFIP transitions subsidized rates toward actuarially sound pricing, meaning your costs will not spike unpredictably. The mandatory 30-day waiting period applies to all new NFIP policies, so you should purchase now-before October’s rainy season arrives-to ensure coverage activates before your actual exposure peaks. An Elevation Certificate from a licensed surveyor documents your building’s height relative to flood levels and frequently unlocks premium reductions of 10 to 20 percent.

Moving Forward With Your Coverage Decision

Your next step involves assessing your property’s specific flood risk and comparing quotes from multiple carriers to find the coverage that matches both your exposure and your budget. A licensed agent can guide you through these decisions and help you understand which protection layers suit your situation best.

How to Secure Flood Insurance in Oregon

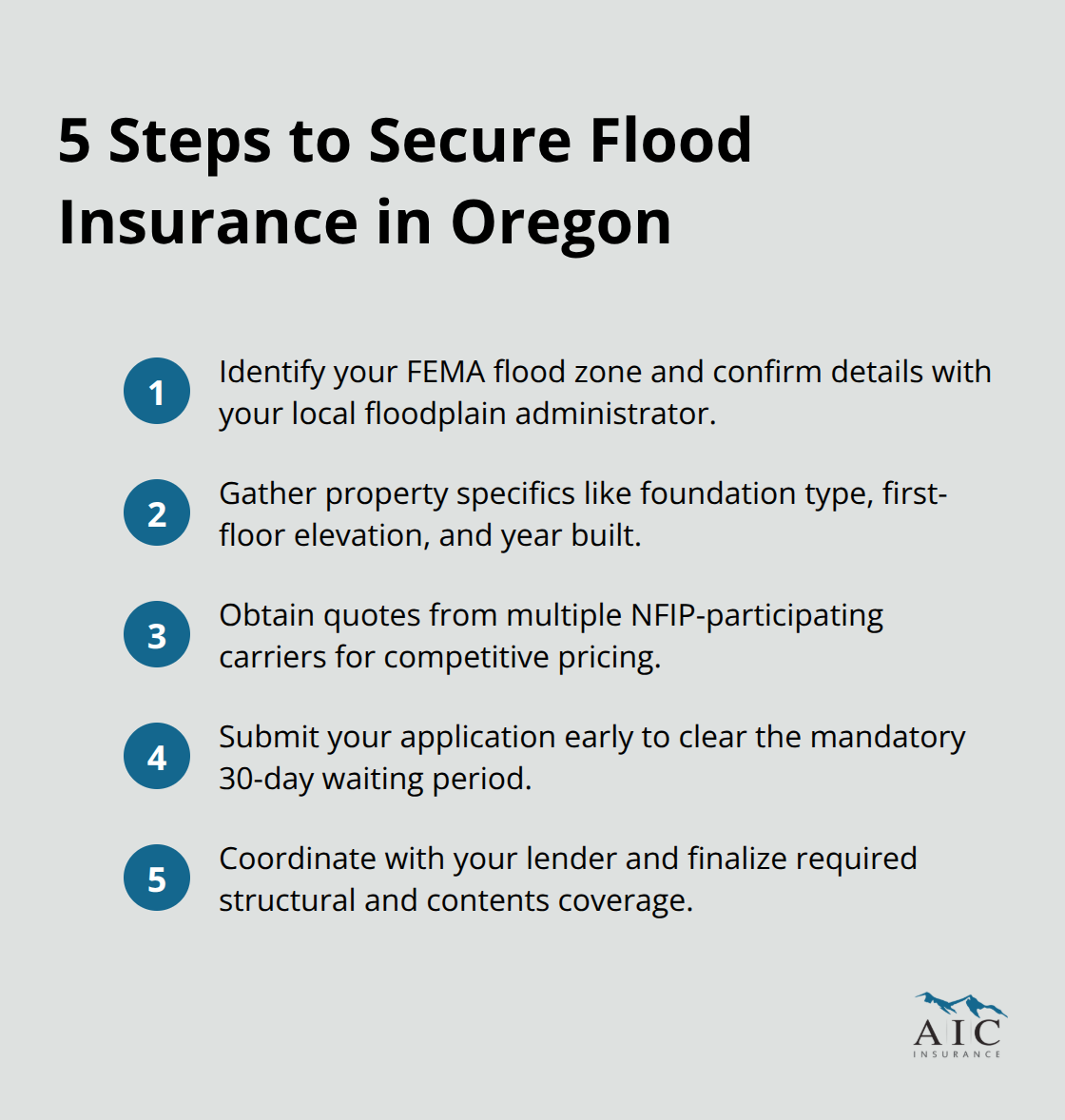

Identify Your Property’s Flood Zone and Risk Level

Start with FEMA’s interactive Flood Hazard Map Viewer to determine whether your property sits in a high-risk A or AE zone, moderate-risk zone, or low-risk area. Your flood zone designation indicates whether insurance is mandatory, strongly recommended, or optional-but the NFIP makes coverage available to all properties regardless of zone, so zone alone should not dictate your decision. Contact your local floodplain administrator in Central Point or your county to confirm your exact designation and request a copy of your Elevation Certificate if one already exists. If no certificate is on file, hire a licensed surveyor to prepare one (typically $300 to $500), which documents your building’s height relative to flood levels and frequently unlocks premium reductions of 10 to 20 percent.

Gather Property Details and Understand Your Premium

Collect your property’s specific information: the year your home was built, foundation type (slab, crawlspace, or basement), first-floor elevation, and replacement cost value of the structure. FEMA’s Risk Rating 2.0 system prices each property individually using these details rather than applying blanket rates by zone. This approach means two homes on the same street can carry dramatically different premiums based on their unique characteristics. Your actual premium reflects your true flood exposure, not just your zone designation.

Obtain Quotes from Multiple Carriers

Contact NFIP-participating carriers-Allstate, American Family, and Auto Club South all operate in Oregon-to request quotes using FEMA’s Get a Quote tool or through direct agent contact. Do not assume all carriers charge identical rates; variation of 15 to 30 percent between insurers on the same property is common because each carrier applies its own underwriting adjustments and operational costs. Shopping multiple providers ensures you find competitive pricing for your specific risk profile.

Complete Your Application Before the Waiting Period Expires

Submit your application immediately once you find coverage that fits your budget, since the mandatory 30-day waiting period begins the moment your application receives approval. This waiting period is non-negotiable across all NFIP policies, making October applications risky-you could face uninsured exposure through November if you wait until late September. Specify both structural coverage (protecting your building up to $250,000 for single-family residences) and contents coverage (protecting personal belongings), which you can adjust based on your actual possessions and risk tolerance. Ensure your policy includes Increased Cost of Compliance coverage up to $30,000, which FEMA includes in all standard policies to cover expenses bringing your home into compliance with current floodplain standards after a flood event.

Coordinate With Your Lender and Secure Final Approval

Work with your lender if you carry a federally backed mortgage; they typically require structural coverage equal to the loan amount, and your servicer may need proof of coverage before the loan closes. An independent agent can walk you through carrier options, explain how your property’s specific characteristics affect your quote, and ensure you understand what each coverage layer protects before you commit to a policy.

Final Thoughts

Flood insurance in Central Oregon protects your home and finances from a genuine and growing threat that extends far beyond mapped high-risk zones. The combination of seasonal snowmelt, intense precipitation, and rapid development affects properties throughout the region, making standard homeowners policies inadequate since they exclude all flood damage. You must act now to secure coverage before October arrives, as the mandatory 30-day waiting period means procrastination leaves you vulnerable during peak flood season.

The steps to securing protection are straightforward: identify your flood zone through FEMA’s mapping tools, gather your property details, obtain quotes from multiple carriers, and submit your application well before the rainy season peaks. An Elevation Certificate documenting your building’s height relative to flood levels frequently reduces premiums by 10 to 20 percent, making this investment worthwhile. NFIP policies include Increased Cost of Compliance coverage up to $30,000, protecting you against the expense of rebuilding to current floodplain standards after a flood event.

Contact AIC Insurance today for personalized guidance on flood insurance in Central Oregon. Our agents understand your region’s specific risks and match you with coverage that protects your property without overpaying for unnecessary limits.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.