Understanding general liability insurance costs is essential for Oregon business owners planning their annual budgets. Your premiums depend on several key factors, from your industry type to your claims history.

This guide walks you through what influences your rates and how to estimate realistic coverage expenses. You’ll also discover practical strategies to lower your premiums without sacrificing protection.

What Drives Your General Liability Costs in Oregon

Industry Classification Sets the Price Foundation

Your industry classification stands as the single strongest predictor of what you will pay for general liability coverage in Oregon. MoneyGeek’s analysis of over 20,000 standardized pricing estimates across Oregon’s insurance market reveals a staggering 13x cost difference between industries. Tech and IT businesses average around $29 per month, while construction and contracting firms pay approximately $388 per month for identical coverage limits. Food and beverage operations typically cost around $146 monthly, healthcare providers around $236, and real estate services near $51. This dramatic variance reflects genuine risk differences: a tech consultant working from home faces minimal third-party injury exposure, while a general contractor operates in high-hazard environments daily.

Oregon’s lack of a cap on non-economic damages since the state Supreme Court’s 2020 ruling further elevates construction and trades pricing, as insurers price in larger potential claim payouts. Your specific operations within your industry matter too-a restaurant with a full kitchen and frequent customer foot traffic carries more risk than a catering business operating primarily off-site, and insurers will adjust your rate accordingly.

Business Size Multiplies Your Exposure and Costs

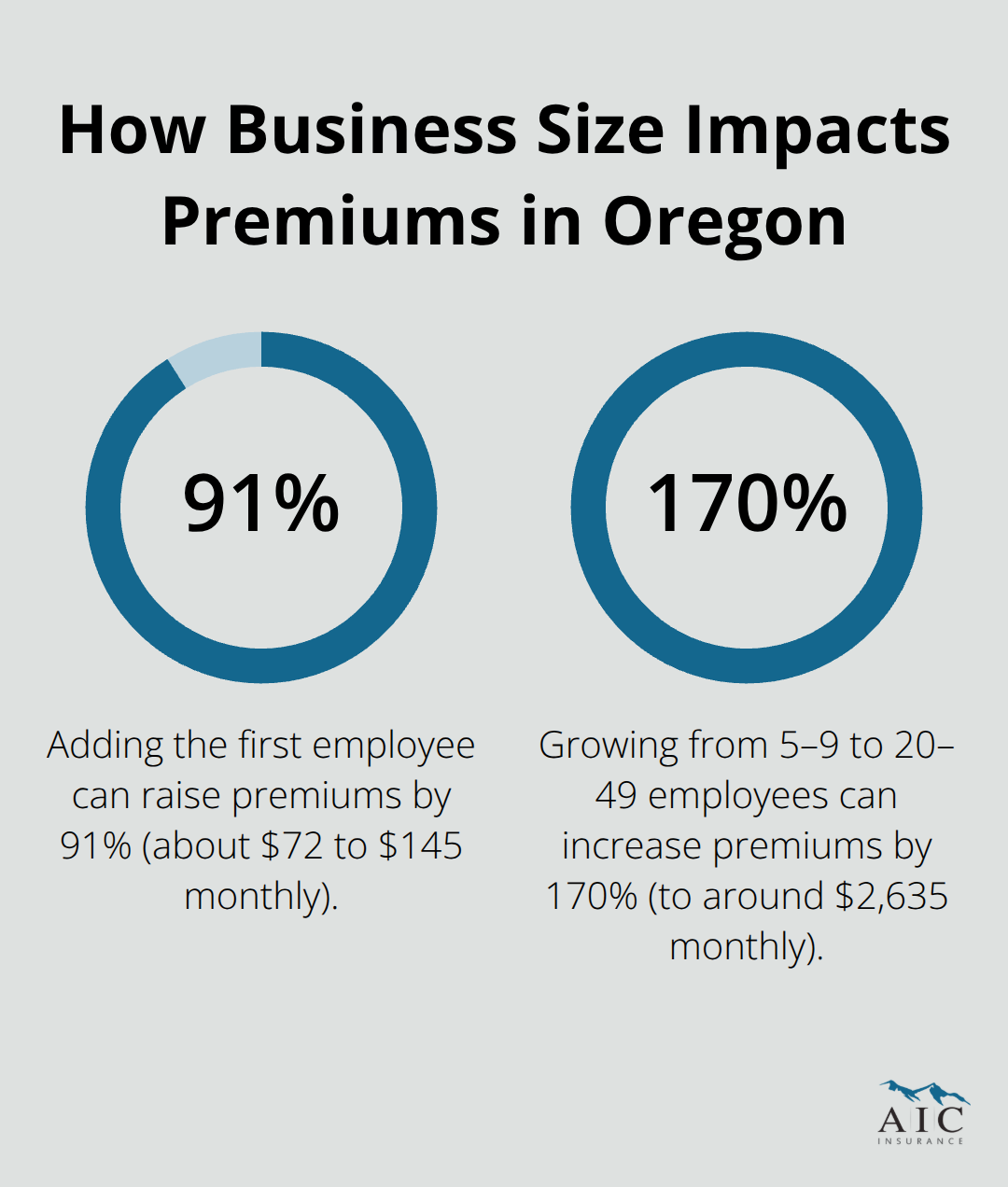

Business size creates equally dramatic cost jumps that most Oregon owners underestimate. Sole proprietors average around $72 monthly, but adding your first employee jumps costs by 91% to roughly $145 monthly. Moving from a 5–9 person team to a 20–49 person operation creates a 170% increase, with firms at that size paying approximately $2,635 monthly.

This isn’t arbitrary-more employees mean more exposure to workplace accidents and third-party claims. Your annual revenue and payroll directly influence how insurers classify your business within your industry, since higher revenue typically correlates with larger operations and greater exposure.

Claims History and Geographic Risk Shape Your Rate

Claims history cuts both ways with brutal efficiency. Filing a claim can raise your insurance premiums for three to five years after the incident. Oregon’s Modified Comparative Negligence Rule means even partially at-fault businesses remain liable, so any claim history-regardless of fault percentage-signals higher risk to underwriters. Geographic location within Oregon also affects pricing; western Oregon’s wet climate increases slip-and-fall exposure for customer-facing businesses, while eastern and southern regions face elevated fire risk pricing for outdoor operations and equipment storage.

Get Quotes to See Your Actual Numbers

Multiple carriers price risk differently, so obtain specific quotes from at least three providers using identical coverage limits and deductibles. This approach reveals exactly how industry classification, business size, claims history, and location compound in your situation-and which carrier offers the best rate for your risk profile.

Building Your Realistic Oregon GL Budget

Start with Oregon’s actual baseline figures, not national averages. Small Oregon businesses with 1–4 employees pay roughly $138 per month ($1,654 yearly) for $1 million per occurrence and $2 million aggregate limits, according to MoneyGeek’s analysis of over 20,000 Oregon pricing estimates. This 12% premium above the national average matters when you budget-Oregon’s lack of non-economic damages caps and its rate-file-and-use system mean prices adjust faster and climb higher than many states. Your specific industry determines whether you sit well below or far above this baseline. Tech consultants in Oregon average $29 monthly while construction firms average $388 monthly for identical coverage. To estimate accurately, identify your exact industry classification and pull quotes from at least three carriers using consistent inputs: the same coverage limits ($1M/$2M), the same deductible, your actual employee count, and your true annual revenue. Different insurers price risk differently, and a $100 monthly difference between carriers for the same protection is common. Comparing apples-to-apples quotes reveals which carrier genuinely offers the best rate versus which one simply quoted you a lower limit or higher deductible. Many Oregon business owners skip this step and overpay by 20–30% annually simply because they accepted the first quote.

Coverage Limits Must Match Your Actual Exposure

Your business size and customer interactions determine minimum coverage needs, not industry averages. A sole proprietor home-based business might operate safely at $1M/$1M limits, but adding even two employees or client site visits should trigger a jump to $1M/$2M. Restaurants typically require higher limits-around $2M/$4M-due to food handling, customer volume, and service liability. Contractors working on residential properties often face contractual requirements for $1M/$2M minimums, sometimes $2M/$2M depending on project value. A single serious claim exhausts your coverage if you underestimate your limits, leaving you personally liable for excess damages. Oregon’s Modified Comparative Negligence Rule means even if you’re 40% at fault, you still face significant exposure. Overestimate and you waste premium dollars on protection you’ll never use. The practical answer is to review your customer contracts first-many specify minimum required coverage-then assess your actual third-party risk based on employee count, work location, and customer interaction frequency.

Riders and Endorsements Add Targeted Protection at Lower Cost

Adding specific endorsements costs far less than blanket limit increases. Product liability endorsements matter for food and beverage operations, manufacturers, and retailers-this separate protection addresses claims from products you sell or distribute, not just services you perform. Liquor liability endorsements protect bars, restaurants, and any business serving alcohol. Pollution liability covers spills, contamination, and environmental claims for operations handling chemicals or hazardous materials. Hired and non-owned auto liability protects you when employees use personal vehicles for business or you rent equipment. Rather than jumping from $1M/$2M to $2M/$4M limits to cover these gaps, add targeted endorsements at 10–25% of the limit-increase cost. Endorsements typically add $10–$30 monthly depending on your operation. This surgical approach to coverage means you’re not overpaying for protection you don’t need while ensuring you don’t skip critical gaps. Work with an independent agent who can map your actual exposures and recommend endorsements rather than accepting a standard package.

Next Steps: Get Quotes That Reflect Your True Risk

The baseline figures and industry examples provide context, but your actual premium depends on your specific situation. Obtain quotes from multiple carriers today using your real business details-your industry classification, employee count, annual revenue, desired coverage limits, and preferred deductible. Each quote reveals how carriers assess your risk differently and which one offers the best value for your protection needs. An independent agent can shop multiple carriers simultaneously, saving you time and ensuring you see genuine rate differences rather than variations in coverage terms.

How to Cut Your General Liability Costs Without Cutting Coverage

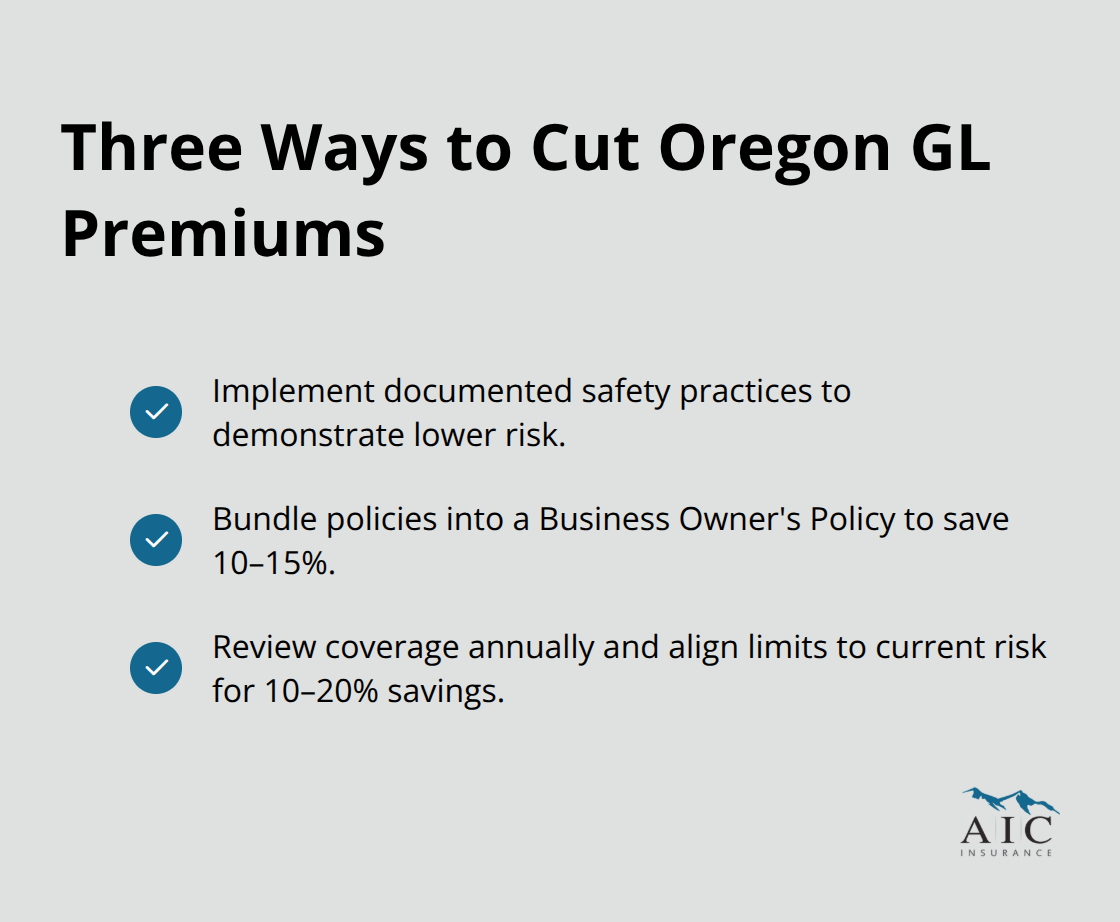

Oregon businesses overpay for general liability insurance because they treat it as a fixed cost rather than a negotiable expense. Three concrete strategies slash premiums without forcing you into inadequate coverage. First, implement documented safety practices that insurers recognize and reward with lower rates. Second, bundle your general liability policy with other coverages into a Business Owner’s Policy, which typically saves 10–15% compared to separate policies. Third, review your coverage annually and adjust limits downward if your business has shrunk or shifted to lower-risk operations-this ongoing calibration prevents you from financing protection you no longer need.

Document Safety Practices to Prove Lower Risk

Start with safety documentation because insurers price risk based on what you can prove about your operations. A written incident reporting procedure, documented safety training logs, and clear protocols for handling customer property demonstrate you take loss prevention seriously. Contractors who maintain certificates of insurance from subcontractors and keep records of on-site safety inspections often see premium reductions at renewal.

Food service businesses that document regular temperature checks, sanitation logs, and staff food-handling certifications position themselves as lower-risk operations than competitors with no paper trail. These practices cost almost nothing to implement but signal to underwriters that your claims frequency should be lower than industry averages.

Bundle Policies to Unlock Multi-Line Discounts

Bundling delivers immediate savings without any operational changes. Most Oregon business owners carry general liability, commercial property, and workers’ compensation as separate policies with different carriers, each charging standalone rates. Consolidating these into a single Business Owner’s Policy with one insurer reduces your total premium because insurers offer multi-line discounts that exceed the cost of individual coverage. An independent agency can show you exactly how much you save through bundling versus staying separate-the difference often exceeds $100 monthly for small operations.

Review Coverage Annually to Match Current Risk

Annual reviews catch premium drift that happens when you keep the same coverage limits year after year despite changed business conditions. If you hired remote staff instead of on-site workers, reduced customer site visits, or exited a high-risk service line, your actual exposure dropped but your premium did not unless you requested an adjustment. Contacting your agent each renewal to discuss whether your $1M/$2M limits still match your true risk-or whether you can safely drop to $1M/$1M-takes thirty minutes and frequently yields 10–20% savings. Oregon’s rate-file-and-use system means carriers adjust pricing frequently, so shopping your renewal with at least two other carriers every two years ensures you avoid paying legacy rates for current risk.

Final Thoughts

Budgeting for general liability insurance costs in Oregon requires you to move beyond national averages and examine your actual business situation. The baseline figures throughout this guide-Oregon’s $138 monthly average for small businesses, the 13x cost spread between industries, and the dramatic jumps tied to employee count-provide essential context for your planning. However, your real premium depends on how industry classification, business size, claims history, and geographic location combine in your specific operation.

An independent agent transforms this complexity into actionable clarity. Unlike captive agents representing single carriers, independent agents access multiple insurers simultaneously and understand how different carriers price your exact risk profile. They identify which endorsements you genuinely need versus which ones waste premium dollars, and they catch coverage gaps that could leave you exposed after a claim.

Gather your business details-industry classification, employee count, annual revenue, desired coverage limits, and preferred deductible-and request quotes from at least three carriers or an independent agent who represents multiple insurers. Comparing apples-to-apples quotes reveals genuine rate differences and ensures you’re not overpaying for the same protection. This process typically saves $50–$150 monthly for Oregon small businesses.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.